As we rapidly approach 2050, an accelerated global zero-emission vehicle (ZEV) transition is crucial to keep the vision of the Paris Agreement within reach. The window for limiting warming to 1.5°C is rapidly closing — the remaining 1.5°C-compatible carbon budget for road vehicles shrank from 84 to 67 billion tonnes between 2020 to 2022, and at the current pace of emissions, will be exhausted by 2030. However, there is reason for optimism.

A recent report by the International Council on Clean Transportation (ICCT) assessed the implications of recent developments from August 2021 to March 2023, including market developments, policies, and international commitments, to take stock of the world’s road vehicle CO2 emissions trajectory. The findings are clear: global momentum on the ZEV transition has accelerated rapidly over the last two years, reducing emissions and bringing the world measurably closer to meeting the upper 2°C limit of the Paris-compatible temperature targets.

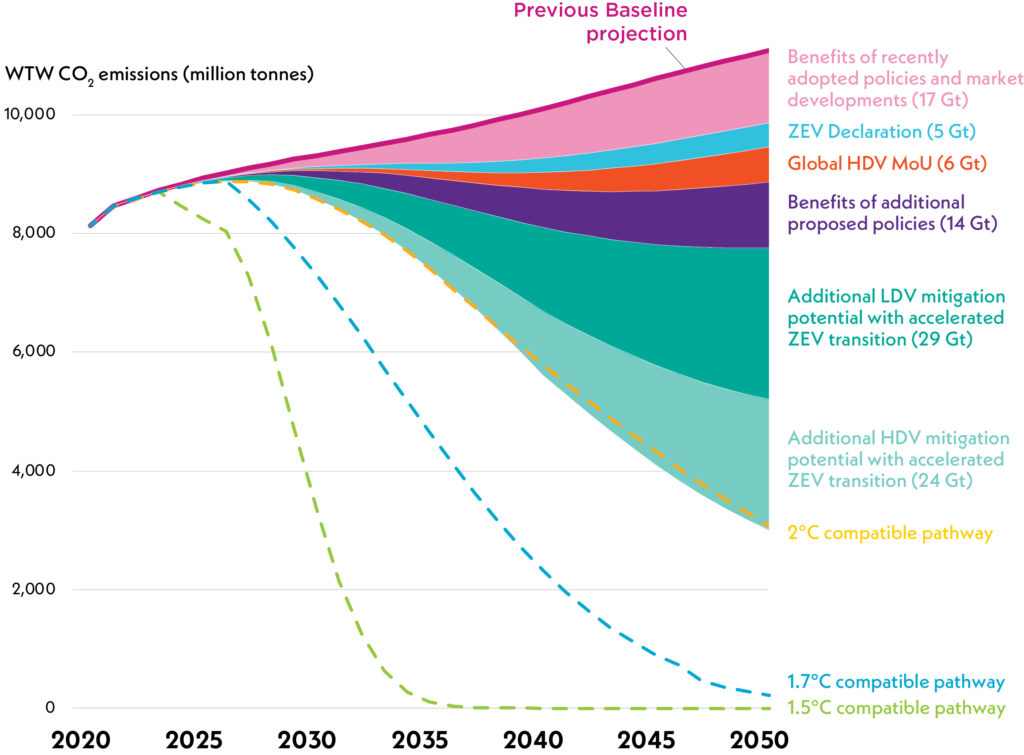

Projected well-to-wheel emissions from road vehicles through 2050

This report incorporates the latest available data on road vehicle sales, stock, and activity; historical global CO2 emissions from road vehicles and other sectors through 2022; considerations of adopted ZEV and electric vehicle (EV) policies and proposed targets; and of the international commitments to the ZEV Declaration, as well as to the Global Memorandum of Understanding on Zero-Emission Medium- and Heavy-Duty Vehicles (Global MOU).

The role of international commitments and national policy

As illustrated in the figure above, international commitments, such as the ZEV Declaration, have a tangible impact on the global outlook. For example, if all 41 national signatories to the ZEV Declaration follow through on their ambitious pledge to reach 100% new sales of zero-emission cars and vans by 2035 in leading markets, and 2040 globally, they could prevent nearly 5 billion tonnes of CO2 from entering the atmosphere. On the heavy-duty side, Global MOU endorsers could avoid roughly 6 billion tonnes.

Combining that with the successful implementation of other domestic EV targets and proposed subnational and national policies, governments around the globe could bend the curve even more, reducing CO2 emissions by 25 billion tonnes through 2050. This is more than the combined 2021 emissions of the world’s top 5 emitters (China, the U.S., India, Russia, and Japan).

Currently, 15 members of the European Union (EU) are signatories of the ZEV Declaration. The car and van CO2 standards adopted in 2023 by the EU, which allow the sale of only zero-CO2 emission vehicles starting in 2035, are expected to avoid another 5.4 billion tonnes of CO2 through 2050. These new standards provide an ideal opportunity for other EU members to sign the Declaration, generating increased momentum and signaling other jurisdictions outside the EU to join the transition. Additionally, California, a subnational signatory to the ZEV Declaration, has paved the way in the United States for an accelerated transition. The recent adoption of its Advanced Clean Cars II, Advanced Clean Trucks, and Advanced Clean Fleets regulations by other U.S. states, together with projected U.S. market growth under recently adopted legislation and regulations, are projected to avoid 8.6 billion tonnes of CO2 emissions through 2050.

Growing momentum to avoid 2°C

We still have a long road ahead—further actions are needed in a much larger set of countries to align the global vehicle fleet with a 2°C-compatible pathway and keep below-2°C pathways within reach. Specifically, if major markets, such as the U.S., China, Europe, and Canada, were to reach 100% ZEVs for sales of new cars and vans by 2035, as outlined in the ZEV Declaration, and new buses and trucks by 2040, as outlined in the Global MOU – and all other countries follow suit within five to ten years – it would put the sector on a pathway consistent with keeping warming below 2°C. To align with this trajectory, ZEVs would need to account for nearly half of new global truck sales by 2030, two-thirds of car and van sales, and three-quarters of bus sales. Aligning the global vehicle fleet with a pathway that avoids overshoot of 1.7°C is still possible but could be endangered by even a few years of delayed action. It is therefore critical to continue to raise the level of policy ambition and align more jurisdictions with the visions articulated in both the ZEV Declaration and the Global MOU.